Table of Contents

- IRS Delays Secure 2.0 Mandatory 401k Catch-up Contributions until 2026 ...

- Catch-Up Contributions Into a Roth 401(k) Isn't a Bad Idea | Kiplinger

- Accounting for Employee after-tax 401k contribution (This is NOT ...

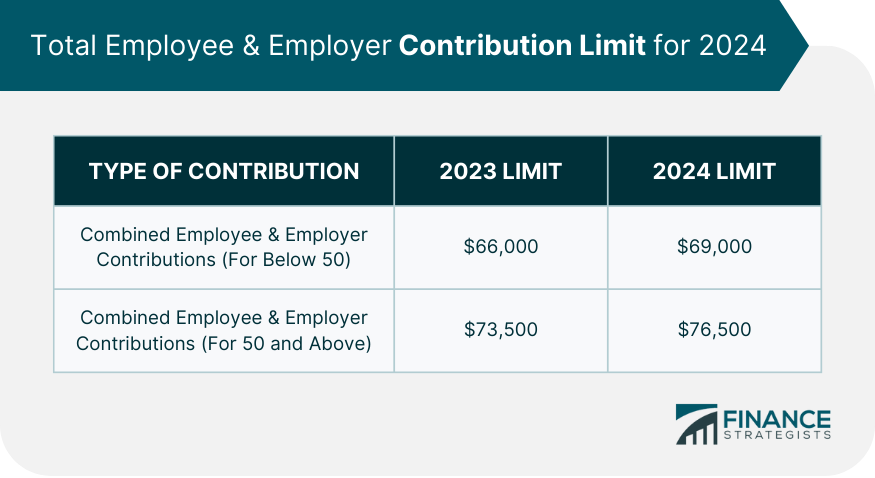

- Maximum 401(k) Contribution for 2025 | Finance Strategists

- Maximum 401(k) Contribution for 2025 | Finance Strategists

- 401(k) Contribution Limits In 2024 And 2025 | Bankrate

- Roth 401(k) employee contribution switched to Traditional contribution ...

- Catch-Up Contributions Into a Roth 401(k) Isn't a Bad Idea | Kiplinger

- Roth 401(k) Contribution Limits for 2025 | Kiplinger

- 2021 401(k) Contribution Limits, Rules, and More

Background: The SECURE Act 2.0

Key Details: Mandatory Roth 401(k) Catch-up Contributions

/401k-contribution-limits-rules-2388221_FINAL-43f987109dd24e6a9d37c24fe2c0a08f.gif)

Implications for Employees and Employers

The mandatory Roth 401(k) catch-up contributions will have significant implications for both employees and employers: Employees: High-income employees will need to consider the tax implications of making Roth catch-up contributions. While these contributions will not reduce their taxable income, they will provide tax-free growth and distributions in retirement. Employers: Plan sponsors must ensure compliance with the new regulation, which may involve updating plan documents, communicating changes to participants, and adjusting payroll processes. The mandatory Roth 401(k) catch-up contributions, set to take effect in January 2025, mark an important change in retirement savings regulations. As the IRS confirms the details of this provision, employees and employers must prepare for the implications. By understanding the key aspects of this change, individuals can make informed decisions about their retirement savings, and plan sponsors can ensure compliance with the new rules. As the retirement landscape continues to evolve, staying informed about these changes is crucial for securing a stable financial future.For more information on the mandatory Roth 401(k) catch-up contributions and how they may impact your retirement savings, consult with a financial advisor or plan sponsor. Stay ahead of the curve and make the most of your retirement planning opportunities.